What is Medicare Supplemental Insurance?

What is Medicare Supplemental Insurance?

Medigap, also known as Medicare Supplemental Insurance, is a private insurance policy that helps cover the out-of-pocket costs that Original Medicare (Parts A and B) doesn't fully pay, such as deductibles, copayments, and coinsurance. Here’s what you need to know:

1. Eligibility

- You must be enrolled in Original Medicare (Part A and Part B) to buy a Medigap policy.

- Medigap is not available for those who are enrolled in Medicare Advantage (Part C) plans. You can only have one or the other.

- You must be at least 65 years old (or disabled and under 65 in some cases) to purchase Medigap.

2. What Medigap Covers

Medigap helps cover some of the following costs not covered by Original Medicare:

- Part A (Hospital Insurance) deductibles and coinsurance.

- Part B (Medical Insurance) coinsurance and copayments.

- Part A and B excess charges (in some cases).

- First 3 pints of blood needed for a medical procedure.

- Some plans cover foreign travel emergency medical expenses, up to a certain limit.

However, Medigap does not cover:

- Long-term care (e.g., nursing home care).

- Vision or dental care.

- Hearing aids.

- Private-duty nursing.

- Prescription drugs (you need a separate Medicare Part D plan for prescription drug coverage).

3. Types of Medigap Plans

There are 10 standardized Medigap plans (labeled A through N) available to new Medicare beneficiaries. Each plan offers a different level of coverage. The benefits are the same across all insurance companies, but the premiums may vary.

- Plan F and Plan G offer comprehensive coverage, covering most of your out-of-pocket costs. However, Plan F is no longer available to new enrollees as of 2020.

- Other plans, like Plan N and Plan K, offer more limited coverage but come with lower premiums.

4. Costs

- Premiums: You’ll pay a monthly premium for Medigap in addition to your Medicare Part B premium. The cost varies depending on the plan you choose, the insurance company, and where you live.

- Medigap premiums can increase over time due to factors like inflation, age, or changes in insurance policies.

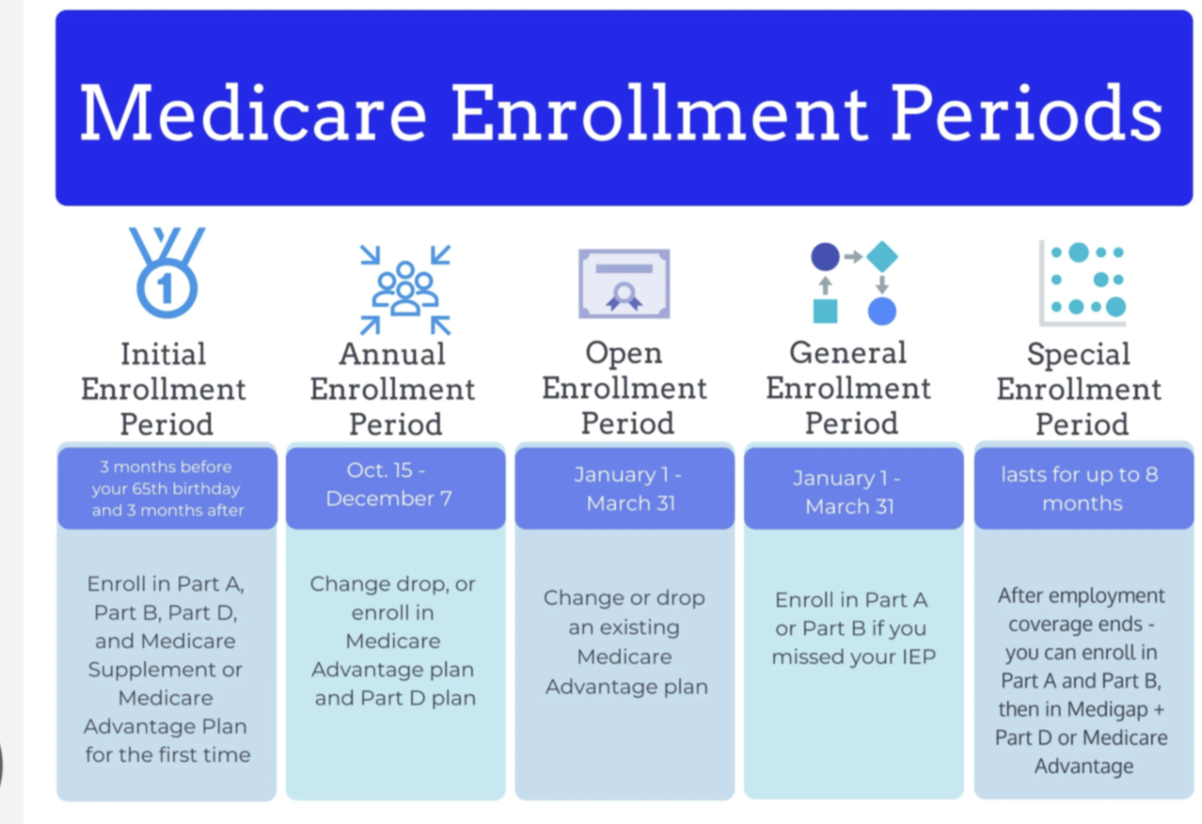

5. Enrollment

- The best time to enroll in Medigap is during your Medigap Open Enrollment Period. This six-month period starts the first month you’re 65 or older and enrolled in Medicare Part B. During this time, you have guaranteed issue rights, meaning you can buy any Medigap plan without being denied coverage or charged higher premiums due to pre-existing health conditions.

- If you apply for Medigap outside of this period, you may be subject to medical underwriting, which could result in higher premiums or denial of coverage based on your health history.

6. Medigap vs. Medicare Advantage

- Medigap works only with Original Medicare, so if you have Medicare Advantage, you cannot have Medigap. Medicare Advantage plans often include additional benefits, such as vision, dental, and prescription drug coverage, but Medigap focuses solely on covering gaps in Original Medicare.

- Medigap helps with out-of-pocket costs for Original Medicare, but Medicare Advantage plans typically have lower premiums and include more comprehensive coverage, though they might also involve network restrictions.

7. Plan Availability and Providers

- Medigap policies are sold by private insurance companies. While the benefits of each plan are standardized, the cost can vary between insurance companies, so it’s important to compare premiums, coverage, and services when choosing a provider.

- Make sure the plan you choose is available in your state. Some plans may not be offered in all areas.

8. Limitations of Medigap

- Medigap does not cover prescription drugs. For prescription drug coverage, you need a Medicare Part D plan.

- Medigap plans have a set coverage structure and don't offer additional benefits like dental, vision, or hearing coverage, unless specified by a plan.

- You can only have one Medigap policy at a time, and it must cover your Medicare Part A and Part B benefits.

9. Switching Medigap Plans

- You can switch Medigap plans at any time, but if you do so outside of the Medigap Open Enrollment Period, you may need to undergo medical underwriting, which could result in higher premiums or denial based on your health.

- It's best to review your plan annually to make sure it continues to meet your needs.

10. How Medigap Helps

- Predictable costs: By covering many out-of-pocket expenses, Medigap can help reduce the financial uncertainty of healthcare costs.

- Freedom to choose providers: With Medigap, you don’t have to worry about network restrictions, unlike Medicare Advantage plans. You can see any doctor or healthcare provider that accepts Medicare.

Conclusion:

Medigap provides valuable coverage for those enrolled in Original Medicare by covering gaps in medical costs. If you're eligible for Medicare and want more predictable out-of-pocket costs, Medigap can help. It’s important to understand when to apply, what plans are available, and how it works with your overall Medicare coverage.

Licensed Insurance Agency

Not connected with or endorsed by the United States government or the federal Medicare program.

We do not offer every plan available in your area. Any information we provide is limited to those plans we offer in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

Medicare has neither reviewed nor endorsed this information. Not connected with or endorsed by the United States government or the federal Medicare program.